The stock market is about to sell off, with major US indexes such as Nasdaq-100 and go Dow Jones industrial average is down more than 10% from their record high since March 30. The ongoing political conflict in the Middle East has sent oil prices soaring, fueling fears of a recession here in the US.

But one stock began to sink long before the war in the Middle East began. Oracle (ORCL +0.79%) has built some of the world’s best data centers for developing artificial intelligence (AI), and demand for its resources is through the roof. However, investors are concerned about the company’s mounting debt, and the credibility of one of its biggest customers.

Oracle stock peaked at about $328 last September, and has since fallen 57%. In another widely used value metric, the stock is already in the lowest price range since the AI boom started gathering in early 2023, so could this be a buying opportunity for investors?

Image source: The Motley Fool.

A leader in AI fundamentals

Most AI development takes place in large, centralized data centers, equipped with thousands of specialized chips called graphics processing units (GPUs). Most businesses don’t have billions of dollars to build infrastructure in-house, so they rent computing power from cloud providers like Oracle.

Oracle data centers are highly efficient, so they require very little human labor to operate, which allows the company to bring them online quickly after construction. Also, every Oracle data center uses digital signal processing (RDMA) technology, designed for advanced AI tasks. It offers low latency and high throughput, thereby moving information between chips and devices faster, and with less data loss, than traditional Ethernet networks.

Most AI developers pay for cloud computing power by the minute, so automated tools that offer faster processing speeds can result in significant cost savings over time.

Scale is another benefit of Oracle tools. It allows its customers to tap into a vast array of over 131,000 GPUs from leading vendors such as Nvidia and Advanced Micro Devicesso they can outrun even the strongest AI models.

A lagging record, but there is an infection

Oracle generated $ 17.2 billion in total revenue during the third quarter of 2026 fiscal year (ended Feb. 28), which was 22% from the previous year. However, revenue from the Oracle Cloud Infrastructure segment increased 84% to $4.9 billion.

Like many cloud providers, Oracle has a greater demand for computing capacity than it can supply, with top AI companies such as OpenAI, Cohere, Meta Platformsand Elon Musk’s xAI that adapts to use its own data centers. As a result, the company ended the third quarter with a staggering $553 billion in remaining operating obligations (RPO), which rose 325% from last year. RPO shows the value of signed contracts for services that have not yet been delivered and is therefore similar to order backlog.

Modern Change

(0.79%) $1.15

Current Price

$146.38

Important Information Points

Market Cap

$418B

Location of the Sun

$140.30 – $146.44

52wk Range

$118.86 – $345.72

Volume

14M

Avg Vol

27M

Gross Margin

64.30%

Separation Products

1.38%

But the devil is in the details. As I mentioned earlier, Oracle stock peaked in September, when did it happen The Wall Street Journal reported that $300 billion of the company’s RPO was generated by ChatGPT developer OpenAI alone. This high number is a problem, because OpenAI has only 25 billion dollars in annual revenue and is seeing huge losses. As such, it is unclear whether the startup will fulfill its large commitment to lease computing capacity from Oracle.

OpenAI recently raised $120 billion in new funding from investors, but even that doesn’t come close to covering its commitments, especially since Oracle is one of the few cloud providers the startup is working with.

To make matters worse, Oracle is carrying more than $124 billion in long-term debt, and is continuing to borrow more to finance the construction of new AI data centers. If major customers like OpenAI don’t come along, Oracle could be in dire financial straits a few years from now.

Is this a good time to buy Oracle stock?

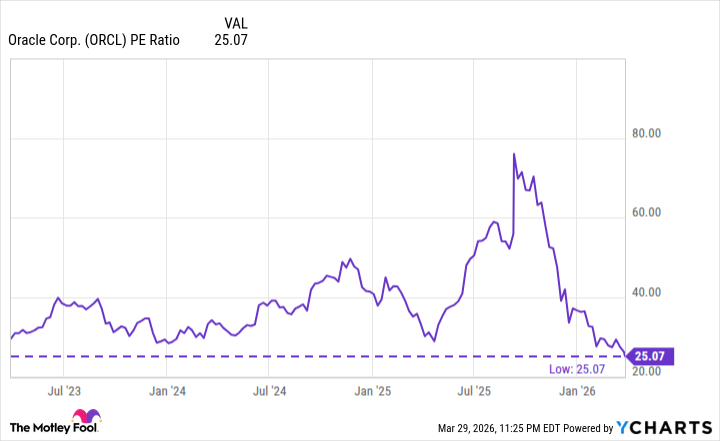

Oracle reported earnings of $5.57 per share over the past four quarters, placing its stock at a price-to-earnings (P/E) ratio of just 25.1. That’s the lowest level in three years:

ORCL PE Ratio data by YCharts

In fact, Oracle stock trades at a discount to the Nasdaq-100 index, with a P/E ratio of 29.9. In other words, it may be undervalued compared to a basket of its major technology peers. But it’s not an outright stock that isn’t always cheap or valuable, so I don’t think the high price is enough to make this stock a buy.

Oracle appears to be more vulnerable than most of its competitors in the cloud computing space due to its heavy debt and the nature of its backlog. Although the company is not directly affected by the conflict in the Middle East, an economic downturn that affects the use of AI everywhere could have a negative impact on its business.

As a result, although Oracle’s long-term outlook may be better than the decline in the stock price, investors may be better off waiting on the sidelines until the broader market stabilizes.

#Oracle #Stock #Hasnt #Cheaper #Years #Buy #Motley #Fool